USD • NASDAQ • Technology

NVIDIA Stock Analysis

2026 Analysis

About NVIDIA

NVIDIA has evolved from a GPU manufacturer into the critical infrastructure layer of the AI economy. Its chips are no longer just components — they are the foundation on which modern AI models are trained and deployed, giving the company a level of pricing power rarely seen in semiconductors.

The business is now overwhelmingly driven by Data Center revenue, which accounts for the vast majority of growth and profit. Flagship systems like H100 and Blackwell are not sold as standalone chips, but as integrated platforms combining hardware, networking, and software. This full-stack approach, anchored by CUDA, creates high switching costs and effectively locks customers into NVIDIA’s ecosystem.

Financially, NVIDIA operates at a level that breaks typical semiconductor benchmarks: revenue growth has exceeded 100% year-over-year, with gross margins above 70%. The market is pricing this as durable, not cyclical. At ~35–45x forward earnings, the stock is expensive — and deliberately so. This is not a mispricing; it reflects the assumption that NVIDIA remains the dominant supplier in an AI buildout that is still in its early innings.

That assumption is where the tension lies — and it leads to a clear conclusion: NVIDIA is overvalued. The current valuation already embeds continued hypergrowth, sustained margins, and minimal competitive erosion. For upside to exist, reality must exceed near-perfect expectations — a narrow path for a company already operating at peak efficiency.

NVIDIA stock snapshot

Revenue growth

Profitability

Valuation

Dividend

Risk level

Medium

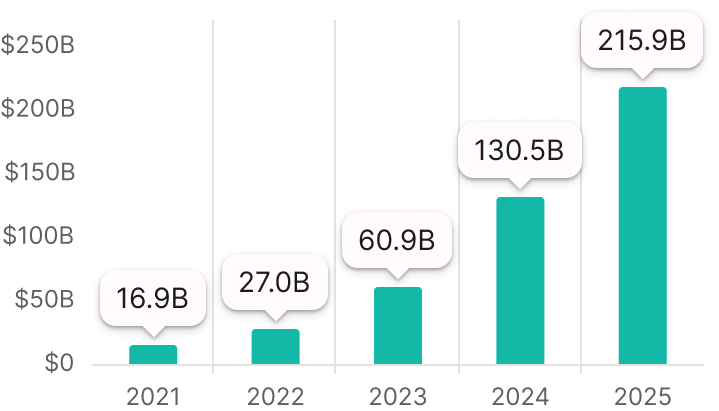

NVIDIA revenue growth

NVIDIA’s growth profile is not just strong — it is extreme by any historical semiconductor standard. A ~35% 5-year CAGR masks what actually matters: recent growth has accelerated sharply into triple digits, driven almost entirely by AI infrastructure spending.

-

Revenue CAGR (5y): ~35%

-

Last 12 months revenue: $37.5B

This is no longer a diversified growth story. Data Center revenue dominates and dictates the trajectory, with hyperscalers like Microsoft, Amazon, and Google deploying billions into AI clusters. Demand is not organic — it is capex-driven, concentrated, and front-loaded. That distinction matters: it pulls future demand into the present.

The market is pricing this surge as durable. At current multiples, investors are assuming sustained high double-digit growth even as comparisons become structurally harder. That assumption breaks under scrutiny: AI infrastructure spending will normalize once initial capacity is built, and growth will decelerate as customers shift from training to optimization and utilization.

To justify the valuation, NVIDIA must continuously unlock new demand layers — inference at scale, enterprise AI adoption beyond hyperscalers, and recurring software revenue through CUDA and AI services. If growth reverts toward even 20–30%, the current multiple compresses aggressively. Conclusion: the growth is real, but the market is paying for a continuation that is unlikely to persist — the stock is overvalued.

Why is revenue growth relevant?

Revenue growth is one of the most critical indicators of a company’s long-term performance, showing how well it can expand its business and capture market opportunities.

NVIDIA Revenue

NVIDIA profit margins

NVIDIA is operating at profitability levels rarely seen in hardware businesses. With ~75% gross margins, ~55% operating margins, and ~49% net margins, this is not typical semiconductor economics — it is platform-level pricing power driven by AI demand.

These margins are not just a function of superior chips. They are sustained by tight supply, bundled systems (compute + networking), and CUDA lock-in, which limits substitution and allows NVIDIA to price for urgency, not cost. Hyperscalers are not optimizing for price — they are optimizing for access.

The market treats these margins as durable. At ~35–45x forward earnings, investors are underwriting a scenario where AI infrastructure remains supply-constrained and NVIDIA retains full pricing control. That is an aggressive assumption. As capacity expands and customers deploy alternatives like custom silicon (TPUs, AWS Trainium) and AMD accelerators, pricing will face pressure.

To justify current valuation, NVIDIA must hold margins above 60% gross while scaling revenue — a combination that requires continued scarcity and zero pricing erosion. The downside is asymmetric: a 5–10 point margin compression would materially impact earnings and force multiple contraction. Conclusion: margins are exceptional, but they are being capitalized as permanent — the stock is overvalued.

Profitability verdict

Current margins imply structural dominance, not cyclical advantage. If AI demand shifts from buildout to optimization, pricing power weakens and margins compress.

The valuation already assumes stability at peak levels — leaving no buffer if customers diversify suppliers or reduce urgency in spending.

Why are profit margins relevant?

Profit margins are a key indicator of a company’s efficiency and competitive strength. They show how much profit a company generates from its revenue after accounting for production costs, operating expenses, and taxes. Companies with consistently high margins typically benefit from strong pricing power, differentiated products, and a durable competitive advantage.

NVIDIA key profitability metrics

Gross Margin

~75%Operating Margin

~55%Net Margin

~49%Profitability verdict

Exceptionally Strong

NVIDIA valuation metrics

NVIDIA is not just trading at a premium — it is priced for near-perfect execution. At ~43–46× earnings versus an industry range of ~25–30×, the market is assigning a structural, not cyclical, advantage to its AI dominance.

The compression to a ~26× forward P/E is often cited as justification, but this is entirely dependent on extraordinary earnings expansion already forecasted by analysts. The multiple is not cheap — it is backward-looking optimism embedded into forward estimates. At the same time, P/S above 20 and P/FCF above 50 signal that investors are still paying aggressively for each incremental dollar of output.

The valuation implies a specific outcome: sustained hypergrowth, stable ~70%+ gross margins, and continued hyperscaler capex at elevated levels. That is a narrow path. A shift in spending toward efficiency, or increased adoption of in-house chips like Google TPUs and AWS Trainium, directly challenges both volume growth and pricing power.

| Metric | NVIDIA | Industry |

|---|---|---|

| P/E Ratio | ~43–46 | ~25–30 |

| Net Margin | ~49% | ~20–25% |

| Revenue CAGR (5y) | ~35% | ~10–15% |

Valuation verdict

The current price assumes NVIDIA remains the uncontested backbone of AI infrastructure while scaling revenue at rates rarely sustained in hardware.

To justify this, AI demand must expand beyond hyperscalers into enterprise at scale, while margins hold near peak levels despite rising supply.

If growth normalizes or pricing power weakens, multiple compression becomes unavoidable.

Conclusion: the valuation already discounts an exceptional future — the stock is overvalued.

Why looking at valuation metrics?

Valuation ratios help investors understand how much the market is paying for a company’s earnings, revenue, and cash flow.

NVIDIA key valuation metrics

Average P/E (5y)

~60+P/E ratio

~43–46Forward P/E

~26Price-to-Sales

~23–26Price-to-Free-Cash-Flow

~52–57Valuation verdict

Expensive to industry

NVIDIA dividend analysis

NVIDIA’s capital allocation sends a clear signal: every dollar is more valuable reinvested than returned. With a ~0.02% yield and ~1% payout ratio, the dividend is economically irrelevant — it exists for signaling, not income.

This is rational given the return profile. NVIDIA is deploying capital into AI accelerators, networking (InfiniBand), and full-stack systems where demand remains supply-constrained and margins exceed 70% gross. Reinvesting at these returns compounds value faster than any distribution policy.

The market endorses this choice by assigning a ~43–46× P/E and >50× P/FCF. Investors are not paying for yield — they are paying for continued high-return reinvestment at scale. The dividend, even growing at ~20% CAGR, does not move the thesis.

What needs to go right is precise: incremental capital must keep earning outsized returns through sustained AI capex, expansion into inference workloads, and monetization layers on top of CUDA. If returns on reinvested capital compress — due to hyperscaler in-house chips (TPUs, Trainium) or a shift from buildout to utilization — excess cash will rise and the absence of meaningful payouts becomes a drag on valuation. Conclusion: the dividend policy reinforces a growth narrative already fully priced in — the stock is overvalued.

Dividends analysis

NVIDIA is not an income asset — it is a capital compounding vehicle dependent on reinvestment at exceptional returns.

The risk is structural: if reinvestment opportunities weaken, capital returns must increase, which typically coincides with lower growth and multiple compression.

What dividends tell us?

Dividends are an important factor for investors who want regular income from their investments.

NVIDIA dividends analysis

Dividend Yield

~0.02%Payout Ratio

~0.98%Dividend Growth CAGR (5y)

~20%Dividends analysis

Low dividend payment

Risks Investors Should Watch

NVIDIA’s risk profile is not about survival — it is about failing to meet extreme expectations already embedded in the stock. At ~43–46× earnings and >50× free cash flow, even strong execution can translate into weak returns if reality falls short of perfection. The stock is overvalued, and the downside is driven by expectation resets, not business collapse.

AI Capex Normalization

Current demand is driven by front-loaded hyperscaler spending, not steady-state consumption.

Microsoft, Amazon, and Google are accelerating buildouts now, which pulls forward multiple years of demand into a short window.

When capacity is installed, spending shifts from expansion to utilization — reducing order intensity and compressing growth rates.

Customer Vertical Integration

The largest buyers are actively reducing dependency.

Google TPUs, AWS Trainium, and Microsoft’s custom silicon are not experiments — they are strategic cost controls at scale.

Each percentage point of workload shifted in-house directly erodes NVIDIA’s volume growth and weakens pricing leverage.

Margin Compression from Supply Expansion

Today’s ~75% gross margins are sustained by scarcity.

As supply increases and alternatives improve, pricing shifts from urgency to negotiation.

A 5–10 point decline in gross margin would have an outsized impact on earnings given the current cost structure and expectations.

Valuation Compression Without Fundamental Deterioration

The multiple assumes sustained hypergrowth and peak profitability.

If growth settles into a still-strong 20–30% range, the valuation no longer holds.

Multiple contraction becomes mechanical, even if revenue and earnings continue to rise.

Supply Chain Concentration

NVIDIA depends heavily on TSMC’s advanced nodes for leading-edge production.

Any disruption — capacity constraints, geopolitical tension around Taiwan, or prioritization shifts — directly limits NVIDIA’s ability to convert demand into revenue.

In a business priced for continuous expansion, even temporary supply friction can trigger disproportionate downside.

Final Verdict: Is NVIDIA Stock Overvalued in 2026?

NVIDIA is overvalued. At ~40–45× earnings versus ~25× for the semiconductor industry, the stock is priced as the permanent winner of the AI infrastructure layer, not just a current leader.

The fundamentals are exceptional — ~35% 5-year revenue CAGR and ~49% net margins — but the market is capitalizing these metrics as if they are structurally durable at scale. That assumption ignores the nature of the current cycle: AI demand is driven by concentrated, front-loaded hyperscaler capex, not steady, recurring consumption.

The valuation already assumes what needs to go right: continued hypergrowth, sustained ~70%+ gross margins, and limited share loss to custom silicon. That leaves no margin for error. If growth normalizes toward 20–30% or margins compress even modestly, earnings expansion will not offset multiple contraction.

The upside case requires a second wave: enterprise AI adoption at scale, inference workloads matching training demand, and software monetization through CUDA becoming a meaningful revenue layer. Without this, the current revenue base becomes a peak, not a floor.

Conclusion: NVIDIA remains a category-defining company, but the stock price already reflects an exceptional future — leaving asymmetric downside if reality falls short.

NVIDIA Takeaways

Revenue CAGR (5y)

~35%

Net profit margin

~49%

NVIDIA P/E ratio

~36

Semiconductor industry P/E

~24

Dividend yield

~0.03%

Overall verdict

Overvalued

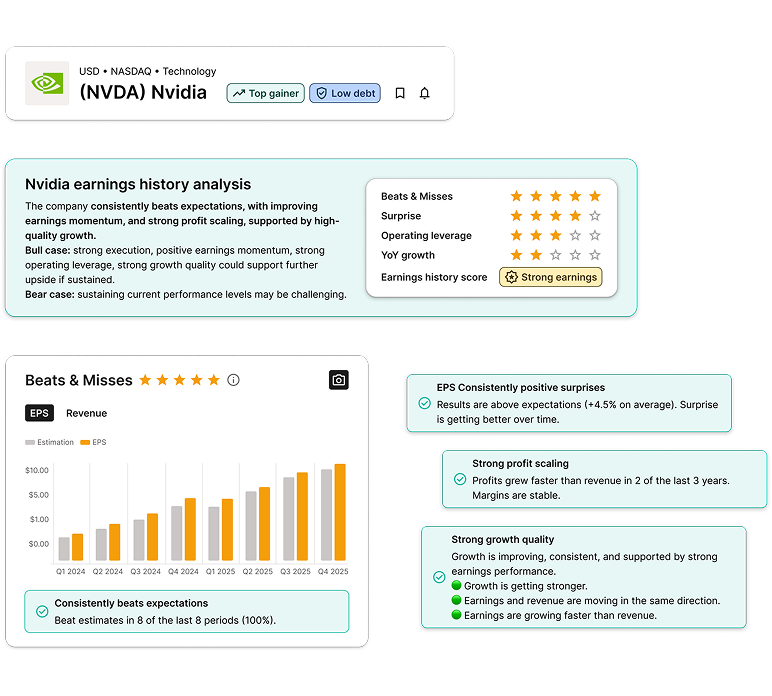

NVIDIA’s earnings history and earnings call reports

High-quality shares are always backed by a proven track record of earnings. Take a look at this company’s earnings performance, our analysis and the key insights from the latest earnings calls.